A liquidity-aware intraday engine built for equity and options microstructure.

QuantEdge Technologies develops institutional-grade trading infrastructure that reads real-time depth, models liquidity behavior at multiple scales, and adapts execution across equity and options markets under changing intraday regimes.

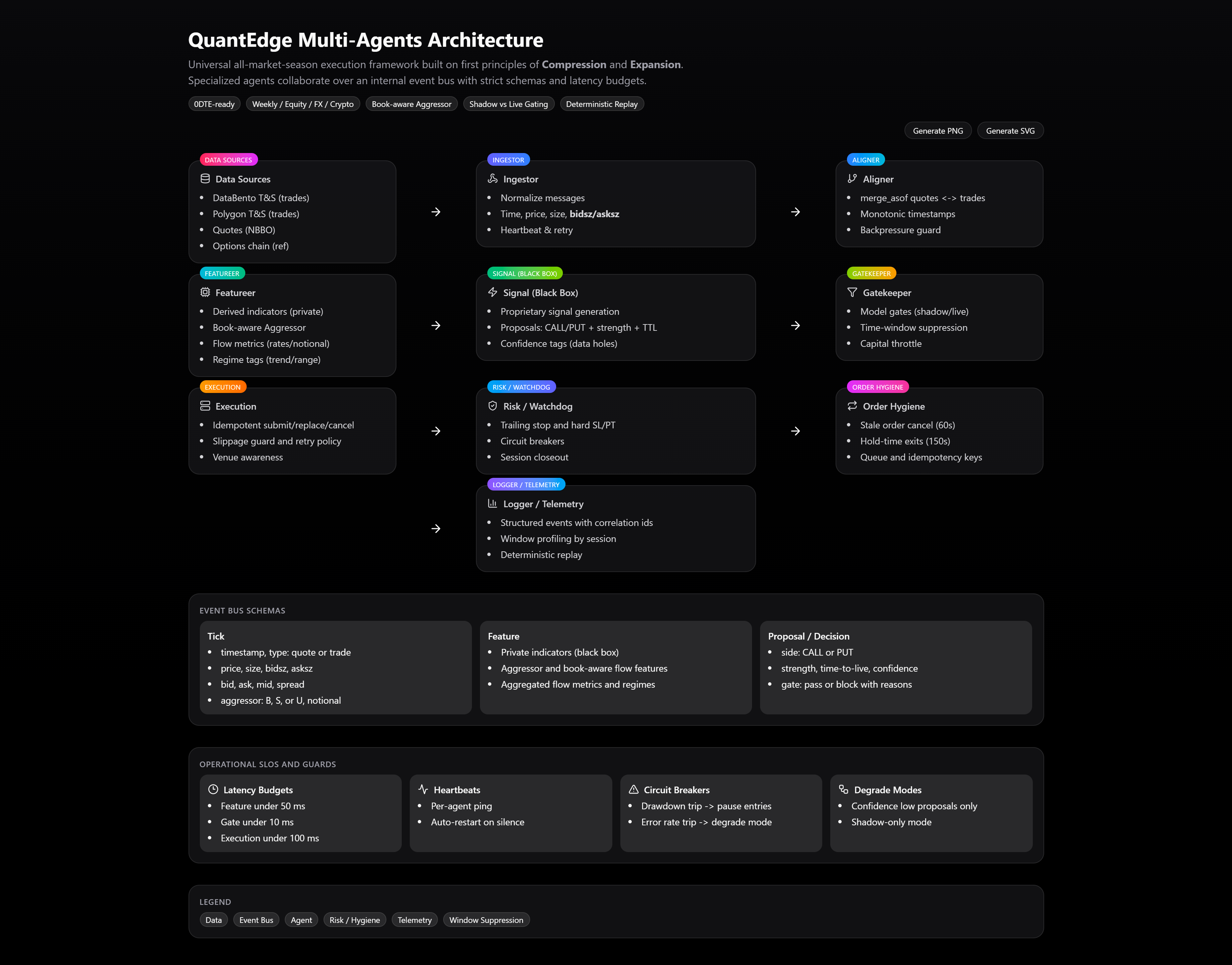

ENGINE ARCHITECTURE

From raw market data to adaptive execution — a layered system built around liquidity, structure, and risk discipline.

Liquidity-first. Structure-aligned. Risk-driven.

The QuantEdge Engine treats equity and options markets as interconnected liquidity environments rather than isolated price series. It aggregates cross-venue depth, models persistent order-book behavior, and adapts execution using regime context and risk-first controls.

- Cross-venue depth aggregation: equity and options DOM across major venues.

- Liquidity modeling: persistence, replenishment, and depletion dynamics.

- Strike-level microstructure context for options and clustered liquidity behavior.

- Intraday regime detection and state-aware execution constraints.

The engine is designed to be understandable by a risk manager as well as an engineer. Every decision path is loggable, auditable, and rooted in observable liquidity and structure— without exposing proprietary scoring or execution logic.

- L1 – Multi-Venue Data Ingestion: real-time equity and options depth feeds.

- L2 – Liquidity Modeling: persistence, imbalance, and strike-level behavior context.

- L3 – Regime & Risk Layer: state machines, protective exits, and constraint-based trading.

- L4 – Execution & Diagnostics: routing safeguards, fill reconciliation, and full-session audit trails.

A simplified view of how QuantEdge processes markets in real time— from cross-venue depth to liquidity-aware, risk-controlled execution.

Market Data Ingest

Equity + options depth, prints, and bars streamed into a unified pipeline.

Cross-Venue Depth Aggregation

DOM updates merged into stable depth views with time-based persistence.

Liquidity Modeling

Imbalance, replenishment, depletion, and strike-level behavior context.

Regime & Risk Layer

State-aware constraints, structural exits, and protective controls in real time.

Execution & Diagnostics

Broker-layer safeguards, fill reconciliation, and full-session auditing.

Research notes & internal experiments.

QuantEdge runs continuous experiments on liquidity microstructure behavior, intraday regime transitions, and signal robustness across instruments and timeframes. This work is exploratory, iterative, and entirely data-driven.

Over time, selected insights will be summarized here as short research notes— not as trade calls, but as documentation of how components behave under stress, and how execution decisions are validated responsibly.

- Price inflection detection vs. traditional indicator crossovers.

- Regime-aware execution vs. static rule sets.

- Microstructure changes around sessions / volatility events.

- Behavior of the stack under different market environments.

This area is under active development. Public research notes will be added once internal experiments reach stable, repeatable conclusions that can be communicated responsibly.

From rockets to tape.

Samuel Banahene is an aerospace engineer by training, working on complex systems and high-stakes environments before building QuantEdge. That same mindset precision, redundancy, and respect for risk is what underpins the engine.